RESEARCH:

Forecasting Volatility with Macroeconomic Sentiment

News sentiment plays a significant role in predicting market volatility. When media coverage turns negative, highlighting risks such as economic downturns, geopolitical tensions, or corporate scandals, investors often anticipate potential losses and adjust their portfolios defensively, leading to increased price fluctuations. This dynamic becomes even more pronounced during unexpected wars or geopolitical shocks.

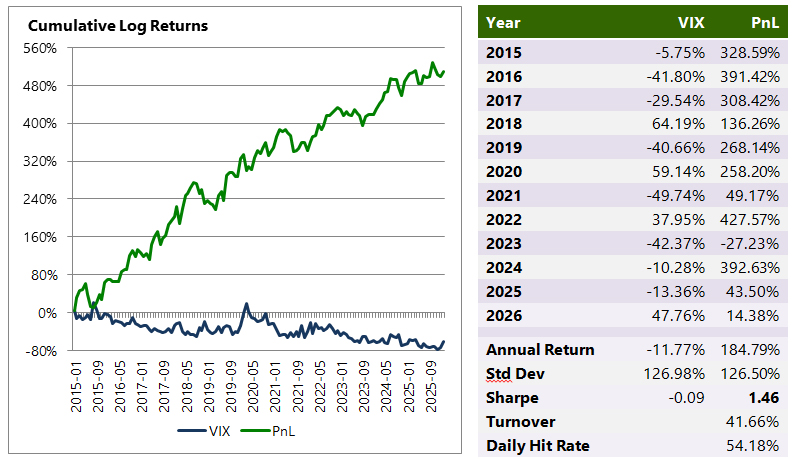

The Dow Jones Institutional Newswire is a multi-asset news feed with over 40,000 news articles published every day. We use Alexandria’s News Analytics to classify economic news for the US into different categories, including inflation and War. We create daily sentiment values for each category and regress the category sentiments (X variables) against daily VIX futures returns (Y variable) using Elastic Net. The in-sample period is a rolling 15 year window where we re-estimate values each year. We then apply the parameters to 2015 to 2025 out-of-sample, achieving a Sharpe Ratio of 1.46.

For more information, request one pager or schedule a call using the request form on the right panel.